crypto payment crypto-wallet cryptocurrency

DAC8 Crypto Tax Guide 2026: Reporting Digital Assets in the EU

- What is DAC8 and who is affected?

- Key Terms to Know

- What is the new directive and how does it change the landscape?

- Which assets fall under digital asset reporting?

- DeFi and Non-Custodial Wallets: The Grey Area

- Compliance vs. Levies: Impact on Different Countries

- Business & Merchants (B2B): What Changes for Acquiring?

- Penalties for Non-Compliance

- Real-Life Use Cases: Understanding Taxable Events

- Step-by-step plan: how to report crypto on taxes in 2026?

- How the Quppy ecosystem simplifies asset control under the new rules

What is DAC8 and who is affected?

What it is: The eighth amendment to the Directive on Administrative Cooperation, requiring Crypto-Asset Service Providers (CASPs) to share user transaction data with European fiscal authorities.

Who is affected: Individuals, legal entities, and merchants residing in the region who conduct transactions with virtual funds.

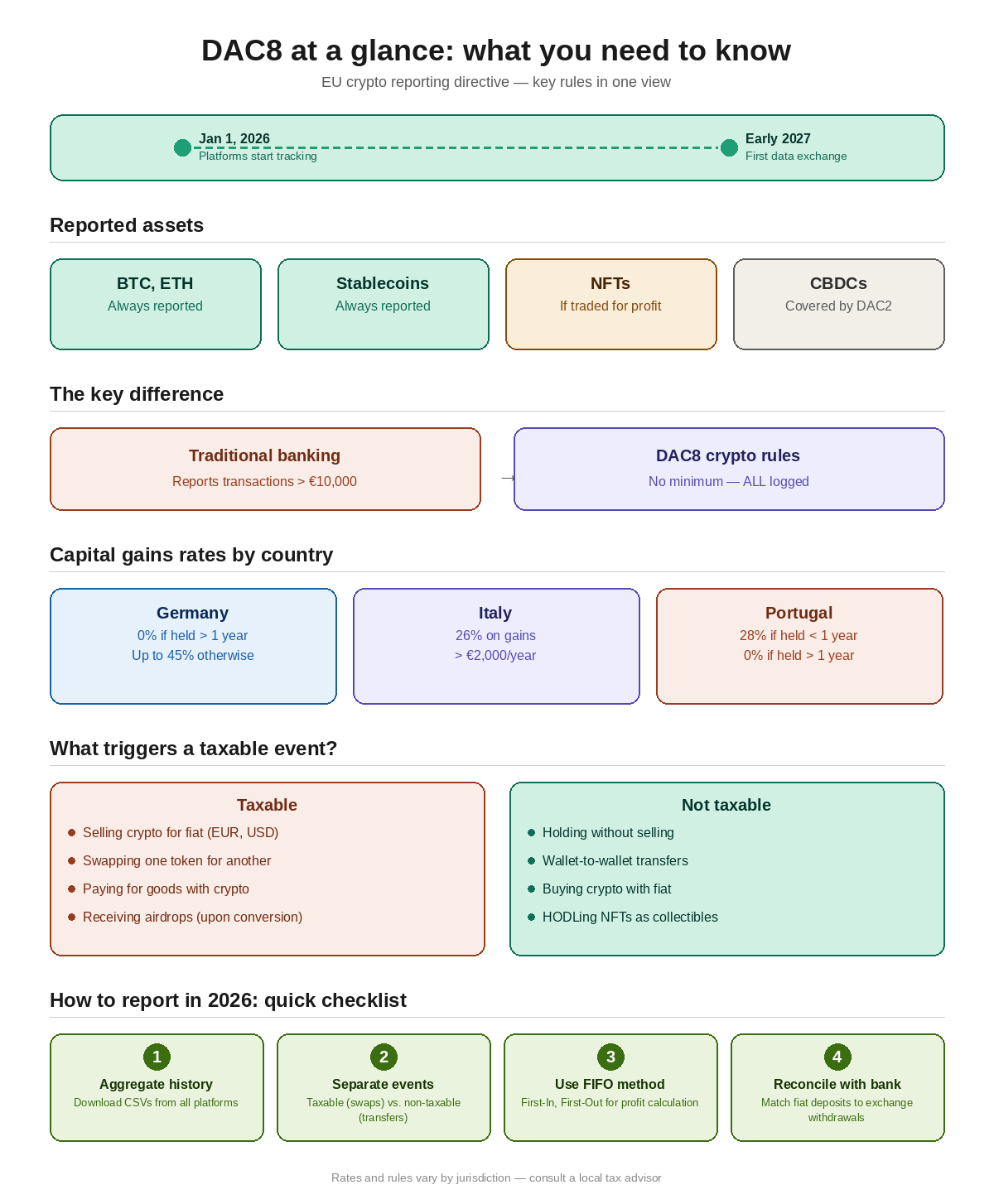

Timeline: The rules officially come into effect on January 1, 2026.

The core objective: To establish an automatic exchange of information between member states, monitor crypto income tax, and prevent financial evasion across borders.

Key Terms to Know

To navigate the new EU crypto regulation landscape, keep these essential terms in mind:

- AEOI (Automatic Exchange of Information): The global standard that allows revenue bodies to automatically share financial data.

- CASP (Crypto-Asset Service Provider): Any regulated platform (exchanges, brokers, custodial wallets) facilitating digital token transfers.

- Loss Harvesting: A legal strategy involving selling coins at a deficit to offset capital gains liabilities.

- KYC / TIN: Know Your Customer procedures and Tax Identification Numbers, which CASPs will now mandate for all users.

What is the new directive and how does it change the landscape?

The European Union is moving away from fragmented local laws toward a unified financial framework. Together with the Markets in Crypto-Assets (MiCA) framework, this amendment represents a massive shift in how decentralized wealth is monitored.

According to the European Commission’s Official Directive on Administrative Cooperation, the burden of tracking digital capital no longer falls solely on the user. Starting in 2026, regulated platforms providing custodial storage or exchange services will automatically submit user balances, transfers, and token-to-fiat conversions.

The “No Minimum Threshold” Rule

A critical difference between traditional fiat banking and the upcoming legislation is the absence of a minimum threshold. While regular banks typically flag transfers exceeding €10,000, digital asset reporting under these new rules requires platforms to log user activity regardless of the transaction size. Every movement is recorded and shared.

Non-EU Exchanges and Global Compliance

Does using an offshore exchange protect your data? No. Under the updated framework, foreign platforms providing services to European residents are also legally required to register and submit transaction data to local authorities. Failure to comply will result in these entities being blacklisted within the Union.

Which assets fall under digital asset reporting?

Not every coin triggers the same obligations. The legislation specifically targets virtual funds used for payment or investment.

| Asset Category | Subject to Rules? | Entity in Charge | Fiscal Implications & Notes |

|---|---|---|---|

| Cryptocurrencies (BTC, ETH) | Yes | Exchange / Wallet Provider | Any tax on bitcoin is usually calculated upon exchanging it for fiat or purchasing goods. |

| Stablecoins (USDT, USDC) | Yes | Exchange / Wallet Provider | Essential for monitoring liquidity movements across borders. |

| Utility Tokens & NFTs | Conditional | Regulated Platform | Logged if traded on centralized exchanges for profit; often ignored if strictly used within a closed app. |

| CBDCs & E-Money | No (Covered by DAC2) | Central/Commercial Banks | Monitored through standard banking directives and fiat gateways. |

DeFi and Non-Custodial Wallets: The Grey Area

A common question among experienced users is how the directive affects DeFi (Decentralized Finfoance) and non-custodial wallets like Ledger or MetaMask.

Since the burden is placed on CASPs, true peer-to-peer transfers between cold wallets do not automatically generate a compliance record. However, the moment you move funds to a regulated exchange to cash out via SEPA transfers, the centralized platform will log the incoming transaction.

Compliance vs. Levies: Impact on Different Countries

It is vital to understand that the amendment harmonizes data collection, not actual rates. The exact crypto income tax you pay still depends heavily on your country of residence.

- Germany: Virtual capital is treated as private money. If you hold an asset for over exactly one year, the sale is duty-free. However, the exchange will still log the transaction, and the BZSt will verify if the 1-year holding period was respected.

- Italy: A 26% levy applies to capital gains exceeding €2,000 per year. The automated summaries will help the Agenzia delle Entrate seamlessly track when users cross this specific threshold.

- Portugal: Previously a haven, Portugal now imposes a 28% rate on capital gains for tokens held for less than a year. The new framework ensures that residents using foreign exchanges cannot hide short-term trading profits.

Business & Merchants (B2B): What Changes for Acquiring?

The legislation doesn’t just affect individual traders; it heavily impacts businesses accepting blockchain payments. E-commerce stores, SaaS platforms, and freelancers receiving B2B settlements in USDT or BTC will have their incoming cash flows monitored.

For businesses, integrating a compliant B2B API or acquiring solution is no longer optional. Using a regulated financial hub like Quppy ensures that all incoming payments are automatically reconciled and converted to fiat with transparent, audit-ready statements, shielding merchants from manual compliance headaches.

Penalties for Non-Compliance

The EU has set strict penalties to ensure adherence to crypto tax reporting standards. Non-compliant CASPs face fines running into millions of euros. For users, failing to declare assets that have already been submitted by a platform will trigger automatic audits, back-payments, and severe financial penalties from local authorities.

Real-Life Use Cases: Understanding Taxable Events

To clarify how the rules apply, let’s look at two common scenarios:

Scenario A: Loss Harvesting. A user bought Bitcoin at €60k and the price dropped to €40k. They sell it to realize the €20k deficit, then buy it back.

Result: The exchange logs the sale. The user can legally use this recorded deficit to offset other capital gains on their annual return.

Scenario B: Buying Coffee with a Virtual Card. A user pays for a €5 coffee using a virtual debit card. The card provider instantly converts Bitcoin to EUR.

Result: This is a reportable event. The conversion triggers capital gains rules, and the transaction is included in the annual compliance summary.

Step-by-step plan: how to report crypto on taxes in 2026?

Preparing for the 2026 fiscal season requires proactive hygiene. If you are wondering how to report crypto on taxes without triggering red flags, follow this checklist:

- Aggregate your history: Download full CSV records covering deposits, withdrawals, and trades across all your platforms.

- Separate liable events: Distinguish between taxable actions (token-to-fiat swaps) and non-taxable actions (wallet-to-wallet transfers).

- Apply the correct accounting method: Most European countries require the FIFO (First-In, First-Out) method to calculate realized profits.

- Reconcile with traditional banking: Ensure that the funds entering your bank account match the withdrawal records from your digital platforms.

How the Quppy ecosystem simplifies asset control under the new rules

Maintaining compliance is difficult when funds are fragmented across dozens of apps. The incoming standards require clear, consolidated financial histories.

Using a unified neobank like Quppy allows you to keep both traditional fiat and digital capital in a single environment. By operating with a dedicated virtual IBAN alongside a secure multi-currency wallet, users can easily track the exact moment an asset moves through a fiat gateway.

Instead of manually matching blockchain hashes with scattered bank statements, users benefit from a consolidated transaction history. Fast SEPA Instant and SWIFT transfers are seamlessly logged alongside exchange operations, making it simple to generate transparent, audit-ready statements for personal accounting or fiscal advisors.

Legal Disclaimer: This article is provided for informational and educational purposes only. It does not constitute official financial, legal, or tax advice. Cryptocurrency taxation laws vary significantly by jurisdiction and are subject to change. Please consult with a certified tax professional or legal advisor in your specific country of residence before making any financial decisions.

FAQ

Yes, but conditionally. NFTs used purely for digital art collection may be exempt, but NFTs traded for investment or airdrops converted to fiat or other tokens will be logged by the CASP

Generally, no. In most countries, merely holding digital assets without realizing a profit (converting to fiat or swapping for another coin) does not trigger a liable event. However, your account balances will still be shared under the AEOI guidelines

While DEXs (like Uniswap) currently operate outside the strict definition of CASPs, you will eventually need to move funds to a centralized gateway or bank account to cash out into fiat, which will immediately trigger compliance protocols

While the first data exchange between revenue bodies will happen in early 2027, platforms will begin tracking and recording user transactions for compliance purposes starting January 1, 2026

Try the free app

Bring digital & fiat together, with no compromise!